- Every restaurant food cost calculator runs on the same formula: (Beginning inventory + purchases − ending inventory) ÷ food sales × 100.

- Most restaurants aim for a food cost of around 28–35%, depending on their concept and service style.

- Theoretical food cost is what you should spend based on recipes and the number of covers sold. Actual food cost is what you did spend. The difference between the two is your variance.

- Around 10–15% of food spend is typically lost to waste in professional kitchens. Unexplained variance is often where that loss sits.

- Stocktakes and spreadsheets show the outcome, not the cause. They tell you what changed, but not why.

- Most waste tracking occurs after ingredients have already been mixed, yielding only category-level estimates. Orbisk captures waste before mixing and identifies over 800 ingredients with around 90% accuracy, enabling traceability of cost changes to specific items and moments.

Most operators know how to calculate food cost percentages, but fewer can explain why it stays higher than it should be. Without that visibility, the same variance between what you should be spending and what you are spending shows up month after month, with nothing specific to act on.

This article covers the key formulas and benchmarks, explains how to calculate and interpret variance, and shows what it takes to close the gap.

Food Cost Percentage Benchmarks by Restaurant Type

A fine-dining restaurant naturally incurs higher food costs than a fast-food restaurant. But other restaurant types can deal with less predictable usage, whether it’s a hotel restaurant juggling à la carte and buffet service or catering kitchens cooking to estimated covers.

The table below shows common food cost ranges by restaurant type, along with the operational issues that can push costs higher than expected.

| Restaurant type | Typical food cost % | How hard costs are to control | What pushes costs up |

| Fine dining | 25–35% | Medium | Expensive ingredients and portion accuracy |

| Casual dining | 28–35% | Medium–high | Inconsistent portions and prep waste |

| Fast casual | 25–32% | Medium | Overproduction during batch prep |

| QSR / fast food | 20–30% | Lower | Waste still happens, but standardisation reduces it |

| Buffet/hotel F&B | 28–40% | High | Food is intentionally overprepared and harder to track |

| Contract / corporate catering | 26–34% | High | Multi-site operations and bulk purchasing create inconsistency |

Benchmarks are useful for giving you a target food cost percentage. They don’t explain why you fall outside your ideal range, or which part of your restaurant operation is driving the problem. The formulas below are the starting point for breaking those problems down and measuring where you’re losing margin.

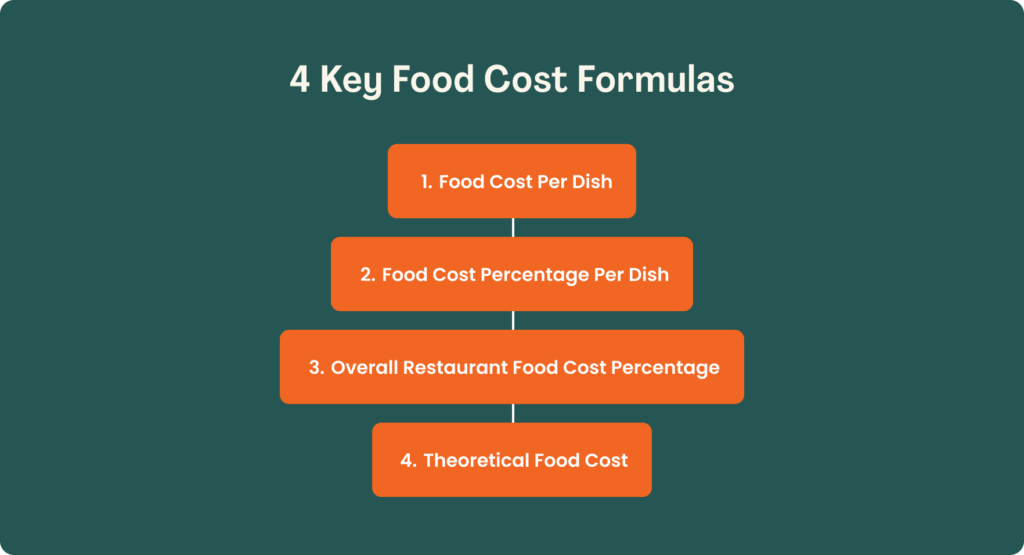

How To Calculate Restaurant Food Cost: 4 Key Food Cost Formulas (With Examples)

Food cost formulas give you a standardised way to measure and manage profit margins. Here are the four most common formulas for calculating a restaurant's food cost.

1. Food Cost Per Dish

The food cost per dish is the total cost of all raw ingredients used to make a single plate. It assumes zero waste and doesn’t include expenses like containers or utensils for takeout dishes.

Food cost per dish = Sum of (ingredient cost per kg ÷ yield %) × portion weight

Most of the calculation sits in the yield adjustment. A chicken breast bought at €8/kg with 85% usable yield actually costs €9.41/kg in usable terms (8 ÷ 0.85). Here’s a worked example of plate costs for a simple chicken dish.

| Ingredient | Purchase price | Yield % | Adjusted cost/kg | Portion | Cost per portion |

| Chicken breast | €8.00/kg | 85% | €9.41 | 200g | €1.88 |

| New potatoes | €1.80/kg | 90% | €2.00 | 150g | €0.30 |

| Green beans | €3.20/kg | 85% | €3.76 | 80g | €0.30 |

| Cream sauce | €4.00/kg | 100% | €4.00 | 60g | €0.24 |

| Total dish cost | €2.72 | ||||

Without yield adjustment, the same dish costs €2.38 on paper. At 80 covers, it becomes €27 of unaccounted cost per service.

2. Food Cost Percentage Per Dish

Food cost percentage per dish tells you what share of a dish’s menu price comes from ingredient cost. It’s used to price new items and check whether existing dishes meet margin targets.

Food cost % per dish = (Food cost per dish ÷ Menu price) × 100

Here’s how to calculate food cost in a restaurant using the chicken dish from the previous example. The food cost per portion is €2.72. If that dish is priced at €9, the food cost percentage is 30.2% (2.72 ÷ 9.00 × 100). To price a new dish, reverse it: divide your target cost by your target percentage.

One limitation of this metric is that it only applies at the individual-dish level. A dish can look correct on paper but still push overall food cost above target if it sells more than expected compared to lower-cost items. When your sales mix shifts, the overall percentage changes even if nothing changes in the kitchen.

3. Overall Restaurant Food Cost Percentage: The COGS (Cost of Goods Sold) Method

This formula measures your actual food cost across the whole business over a given period. Unlike dish-level calculations, it shows what you spent in relation to what you sold.

Food cost % = (Beginning inventory + Purchases − Ending inventory) ÷ Total food sales × 100

Say at the start of the month, a kitchen holds €5,000 of stock. During the month, it buys €18,000 of ingredients. At the end of the month, €4,000 remains. Total food sales for the period are €56,000.

- Step 1: Calculate the total COGS (the cost of the ingredients used to produce the food you sold)

- €5,000 + €18,000 − €4,000 = €19,000

- Step 2: Divide COGS by food sales and multiply by 100

- €19,000 ÷ €56,000 × 100 = 33.9%

In this example, the food cost percentage is 33.9%. For every €1 of food sold, 33.9 cents went on ingredients.

4. Theoretical Food Cost: The Formula Most Operators Underuse

Theoretical food cost is your ideal food cost percentage, or what your kitchen should have spent if every dish was made exactly to the recipe for every meal sold. Unlike the COGS method, which shows what you spent after the fact, theoretical food cost gives you a spending target.

Theoretical food cost % = Σ (Standard recipe cost × Covers sold) ÷ Total food revenue × 100

Σ means "sum of". You calculate the individual recipe cost × covers sold for each dish on the menu, then add the results. Here’s an example for a three-dish menu over one service:

| Dish | Recipe cost | Menu price | Covers sold | Total recipe cost | Total food sales |

| Chicken breast | €2.72 | €9.00 | 45 | €122.40 | €405.00 |

| Salmon fillet | €4.20 | €14.00 | 30 | €126.00 | €420.00 |

| Vegetable risotto | €1.95 | €8.50 | 25 | €48.75 | €212.50 |

| Total | €8.87 | €31.50 | 100 | €297.15 | €1,037.50 |

In this example, you would divide €297.15 by €1,037.50 and multiply it by 100 to reach a theoretical food cost of 28.6%

This is what the kitchen should have spent on these menu items, assuming perfect execution. However, there’s often a difference between how much a kitchen should have spent and what it actually spent.

Start calculating your food cost with Orbisk:

Book a demoActual vs. Theoretical Food Cost: What the Gap Is Really Telling You

Managing the variance between theoretical and actual food costs helps you recover lost profit without additional sales. This section covers how to calculate that gap, what different variance levels mean, and what's most likely causing it.

How To Calculate Your Actual Vs. Theoretical Variance

The COGS method in formula three gives you your actual food cost percentage, or what the kitchen really spent, expressed as a share of food sales. Formula four gives you the theoretical cost: what it should have spent. Subtract the theoretical food cost percentage from the actual food cost percentage to find your variance.

With the figures from the previous examples, that would be 33.9% minus 28.6%, giving a variance of 5.3%. Different variance levels tell you different things about your operational efficiency. Here’s what each range means:

| Variance | What it signals |

| Under 1.5% | Your kitchen is running well. Keep tracking the variance each month and look into it if the gap starts growing. |

| 2–3% | Something is regularly going wrong. Check prep yields, portion sizes on expensive proteins, and whether you're making too much food during certain service periods. |

| 3–5% | There’s a bigger operational problem. Separate waste into categories like overproduction, prep waste, and plate waste. Then compare your theoretical yields with what’s happening in the kitchen. |

| 5%+ | This needs immediate attention. Multiple problems are probably adding up. You’ll need ingredient-level tracking to find the cause because a monthly stocktake alone won’t show where losses are happening. |

That means in our example, a 5.3% variance puts this kitchen in urgent territory. On €56,000 of monthly food sales, that’s nearly €3,000 (5.3% × €56,000) a month the kitchen can't account for.

The Problem With Writing Off Variance As Shrinkage

When your actual food cost runs above theoretical, and you can't explain why, the easiest answer is shrinkage. It's a catch-all term that covers theft, spillage, waste, and anything else that doesn't show up cleanly in the numbers.

The problem is that writing variance off as shrinkage turns a measurable operational problem into a vague accounting category. You know money is disappearing, but not where or why. That makes it difficult to take action or measure whether anything improves next month.

It also hides the scale of the issue. A few missing steaks, inaccurate prep yields, and overproduction at the end of service all create different operational problems, but they appear as the same unexplained loss in your numbers. Without separating those losses, your food cost variance becomes something you accept rather than manage.

The Five Root Causes Of Food Cost Variance

Food cost variance usually results from small operational issues that recur rather than from a single incident. Here are the most common reasons your actual food cost ends up higher than your theoretical food cost.

| Cause | What happens | How it affects your variance |

| Over-portioning | Staff serve larger portions than the recipe calls for | Actual ingredient cost per dish increases while your theoretical cost stays fixed |

| Prep waste and trim loss | The kitchen gets less usable product from an ingredient than the recipe assumes | Your theoretical cost is too low because it's built on the wrong yield, so the gap looks bigger than it is |

| Overproduction | Food is cooked but not sold, and discarded after service | Actual food spend goes up without any matching revenue |

| Spoilage | Ordered stock is discarded before it reaches service | Actual cost rises before service starts, with nothing in the POS data to explain it |

| Voids, comps, and staff meals | Ingredients are used for staff meals, complimentary dishes, or voided orders | The consumption doesn't appear in sales data, so the actual cost is higher than your POS suggests |

Note: Industry data indicate that F&B theft accounts for up to 7% of total losses. It's listed separately because it needs a different response than an operational error. Fixing it requires investigation and access controls, not training or batch size adjustments.

What Waste Stream Really Means, And Why It Matters For Variance

Some of the root causes above show up as physical waste in the bin. A waste stream is how you tell where food waste came from. Here are some examples:

- Overproduction: Food is cooked but not sold and discarded after service. It points to forecasting or batch sizing problems.

- Prep and cutting waste: Product is lost during trimming, portioning, and butchery. It points to gaps in yield calculations in your recipes.

- Plate waste: Food returned to a plate by the guest. It points to portion sizing or menu issues.

- Buffet and service waste: Food is discarded at the end of service. It's the hardest stream to quantify without automated tracking.

Many tracking approaches lump all waste streams into a single food waste figure. But without knowing the specific stream, you won’t be able to tackle the root cause of your variance.

Why Monthly Stocktakes Can't Close Your Variance, And What Can

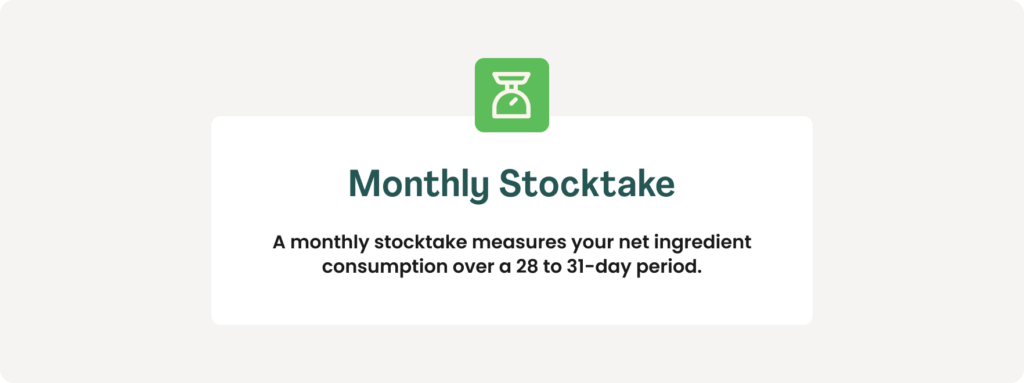

For most kitchens, the default method for investigating variance is the monthly stocktake. The problem is that a stocktake only tells you what you lost, not why it's missing.

What A Monthly Stocktake Measures

A monthly stocktake measures your net ingredient consumption over a 28 to 31-day period. It compares beginning inventory plus purchases against ending inventory to give you your total food cost for the period. Divide that by total food sales, and you have your actual food cost percentage for the month (the COGS formula we covered above).

For example, say following a monthly stocktake, a restaurant finds its actual food cost percentage is running 4% above theoretical. The stocktake confirms the variance exists and roughly what it's costing. But it can't give you anything specific to act on to reduce your variance.

The Data You Need Vs. The Data You Have

Operational data helps you trace any loss back to a specific ingredient, workflow, service period, or kitchen process. Here’s what you need for full visibility:

| What you need | Why it matters |

| Waste by ingredient, not category | "Vegetables: 2kg" doesn't tell you which dish is driving the loss or where in the kitchen it's coming from. Ingredient-level data lets you trace the problem to a specific item and take targeted action. |

| Waste by waste stream | Overproduction and prep waste have different causes and completely different fixes. Without knowing which stream the loss came from, any corrective action is a guess. |

| Waste by shift and station | The same variance figure looks identical whether the problem is happening during Tuesday morning prep or at the end of Friday service. Knowing the shift and station tells you which team to talk to and which workflow to change. |

| Waste at the moment of disposal | By the time a stocktake captures the loss, the context is gone. You know something was wasted: not when, not why, and not whether it's a recurring pattern or a one-off. |

This gap in visibility is why food cost management has traditionally relied so heavily on instinct and experience. Kitchen managers know there’s a problem, but the data usually isn’t detailed enough to show exactly where the loss is happening or which operational change would fix it.

What "Item-Level Waste Data" Looks Like In Practice

Item-level waste data means knowing it was 1kg of salmon, 400g of lettuce, and 100g of lemon rather than “400g vegetables" or "fish prep." Each disposal is recorded by ingredient, station, shift, and cost. That turns a monthly write-off into a real-time picture of exactly what's leaving the kitchen.

Orbisk captures this using image recognition above the bin, before anything mixes. It identifies 800+ ingredients at ~90% accuracy with no input from kitchen staff. Teams throw as normal, and the system records everything automatically.

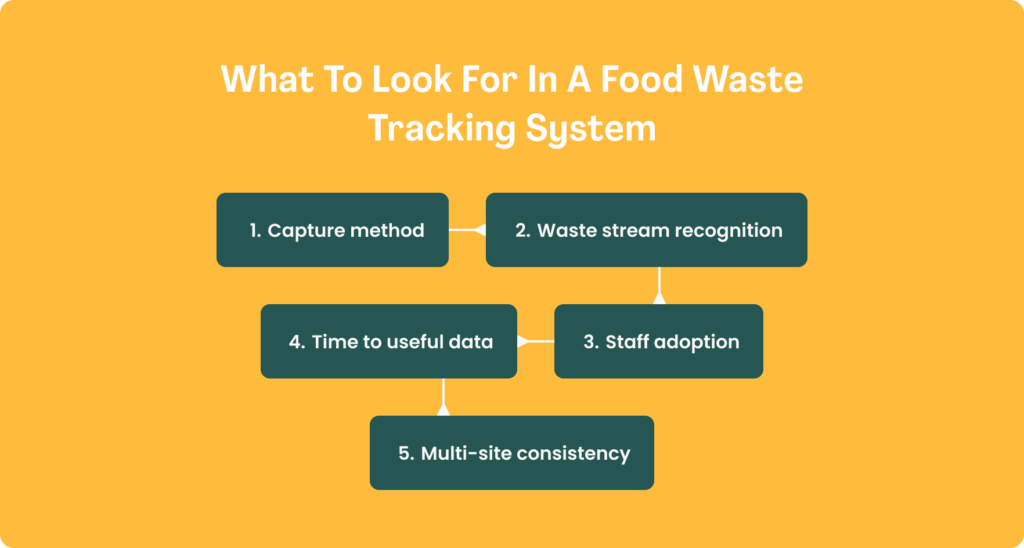

What To Look For If You're Evaluating A Food Waste Tracking System

If you're comparing food waste tracking systems, these criteria determine how well the data will help explain your food cost variance:

- Capture method: Systems that capture food before it hits the bin can identify individual ingredients with much higher accuracy. Once the ingredients mix together, the data becomes broader and less useful for diagnosing variance.

- Waste stream recognition: Automatic tracking is more reliable. If staff need to press buttons or select categories while throwing away food, data quality tends to decline over time.

- Staff adoption: Systems that need training, workflow changes, or waste separation are harder to maintain consistently. Simpler systems tend to produce better long-term data.

- Time to useful data: Some systems need weeks of setup and menu configuration before the data is reliable.

- Multi-site consistency: Using the same tracking method across every kitchen makes it much easier to compare performance between locations.

Once you have the data, you can create a clear plan of action to reduce costs.

3 Operational Moves That Close Food Cost Variance

These three actions target the most common causes of ongoing food cost variance. They don’t require new systems or tools, just a closer look at how your kitchen already works.

1. Check Prep Yield Against Your Theoretical Assumption, Not Just Finished Portions

Most food cost models assume a fixed yield for key ingredients. If your actual yield is lower than that assumption, the difference increases your variance over time. It often goes unnoticed because it looks like normal waste.

To fix this, compare the raw purchase weight to the usable, portioned weight of your highest-cost ingredients. If the yield in practice doesn’t match the yield in your recipes, your theoretical food cost is already off, and every variance based on it will also be wrong.

2. Separate Overproduction From Prep Waste Before Trying To Fix Either

These two problems come from different causes. Overproduction is about forecasting and batch size. Prep waste is about yield or technique.

When they’re grouped together, it’s hard to know what needs fixing. Teams often respond with general training or changes to portion control, even when the real issue is something like outdated batch planning. Once you track them separately, it becomes clear which part of the operation needs attention.

3. Match Ordering To Real Consumption, Not Purchasing Habits

A large part of the food cost variance comes from stock that is ordered but never used. It spoils before service and increases cost without ever appearing on a plate.

To manage this properly, ordering needs to reflect actual ingredient consumption over time, not just what was bought in previous weeks. Most kitchens don’t have that level of visibility. They can see invoices and stocktakes, but not how usage compares to disposal in between.

How Orbisk Closes the Gap Between Your Food Cost Calculation and What's Causing It

The formulas in this article help you calculate your food cost percentage. The variance calculation shows the gap between your theoretical and actual food costs. What those numbers don't show is where the loss is happening inside the kitchen.

A monthly variance report can't tell you that 18kg of salmon was thrown away before Thursday's dinner service. It can't show that your beef prep yield has been below target for the past three months. It can't tell you that overproduction during Sunday brunch is quietly adding hundreds of euros in avoidable costs every week.

That's the gap Orbisk is designed to close.

What Orbisk does

Orbisk works by installing a compact camera above your existing food waste bins. Every time food is discarded, the system captures the disposal before ingredients mix together and before the data disappears.

The system identifies more than 800 ingredients with around 90% accuracy. Then, it tracks waste by ingredient, waste stream, container type, kitchen station, and shift, giving you enough detail to pinpoint the source of losses rather than just the total. Kitchen teams don't need to enter data manually or change the way they work. The system is installed in a single day and runs automatically in the background.

What sets it apart is what happens with that data. Rather than leaving teams to interpret the numbers themselves, Orbisk’s built-in AI analyses waste patterns and surfaces the changes with the greatest potential impact, prioritised and ready to act on.

The result is a live dashboard that shows what's being wasted, when the waste occurs, and where the biggest financial losses come from. Instead of looking at a single unexplained food cost number at the end of the month, teams can see the operational cause of the variance while there's still time to act.

What changes operationally

- Once ingredient-level waste data becomes visible, food cost variance becomes easier to manage. Instead of waiting for a monthly stocktake to reveal a problem, kitchen managers can spot recurring losses during the week and deal with them earlier.

- The system automatically separates different types of waste. Overproduction, prep waste, and spoilage no longer fall under a single broad “shrinkage” category. Each problem can be traced back to a specific process, service period, or kitchen workflow.

- For multi-site operators, the same system runs across every location. Teams no longer rely on inconsistent reporting methods or manual explanations from individual sites. Every kitchen is measured using the same data structure, which makes performance easier to compare and manage across the group.

What the numbers look like

Professional kitchens typically waste between 10% and 15% of their food spend. Once kitchens can see waste at the ingredient level rather than estimating it from stocktakes, Orbisk customers typically recover between 2% and 8% of food cost.

For a kitchen spending €80,000 per month on food, that amounts to roughly €1,600 to €6,400 recovered each month. Orbisk customers typically see up to 70% waste reduction, ROI within four to eight months, and two to ten times return on their investment.

Orbisk is used by more than 1,000 professional kitchens, including Hyatt, Accor, Marriott, and Carnival.

Where to start

Not sure what Orbisk could mean for your kitchen? We show you the dashboard using real examples from kitchens like yours, so you can see exactly how it works in practice. And based on your current data, we calculate what you could save.

No made-up numbers. Just a clearer picture of where your food cost is going and what you can do about it.

See what your variance is really made of:

Book a demoFAQs

This is the COGS method, the most common method for calculating restaurant food cost. It measures what you spent on food relative to what you sold over a set period by calculating the cost of goods sold from your inventory movement and purchases.

Portioning inconsistency is the most common. If kitchen teams are plating slightly more than the recipe specifies, that extra cost builds quickly across a service. Spoilage and untracked waste add further cost that never appears in the recipe calculation.

Old recipe costs are also a common culprit. If ingredient prices have changed but the recipe card hasn't been updated, the theoretical figure will look lower than it should

Each ingredient needs a yield adjustment before you calculate the portion cost. It's also worth adding 3–5% on top to cover minor accompaniments that are difficult to cost individually, like oil or garnishes.

Food cost variance % = Actual food cost % − Theoretical food cost %